(2025-12-08) Green Part3 The Pursuit Of Happiness

Michael Green: Part 3: The Pursuit of Happiness. John Locke, the godfather of liberalism, had a very specific trinity of natural rights: "Life, Liberty, and Property."

For a landed gentry class, this was the ultimate slogan

But Thomas Jefferson did something radical. He took his quill and scratched out "Property." In its place, he wrote: "the pursuit of Happiness."

It was a structural shift in the American operating system driven by Jefferson's mistrust of aristocracy and finance.

he elevated human potential above static accumulation

Happiness""in the Aristotelian sense of eudaimonia"is not about pleasure; it is about flourishing, capacity, and the realization of potential.

By choosing The Pursuit of Happiness, Jefferson prioritized future potential over past accumulation. He chose the worker over the rentier

For much of the last 40 years, the United States has drifted into a nightmare. We have built an economy optimized for Property, not Pursuit. We tax wages (pursuit) heavily, while subsidizing debt and capital gains (property).

In Part 1, we identified the "tree" " the hidden precarity for many American families. ((2025-11-23) Green Poverty Line Is A Lie)

In Part 2, we outlined the "asset lie" for most participants (and supported Part 1) ((2025-11-30) Green Part2 The Door Has Opened)

Today, in Part 3, I promised solutions. I lied. Kinda. I will propose the solutions at the end in a format that allows you to run them through any LLM to test them yourself. Don"t take my word for it. But before we get there, we need a bit more diagnosis to understand what went wrong.

Are We Wrong?

the overwhelming feedback has been, "Yes! This is my "life" and I"m not very happy with it."

This "expert" is not an expert in statistics, but he's clearly heard of the two-axis chart crime that is sweeping the nation. Unfortunately, this led him to commit a different type of error " Variance Masking (or simply a Normalization Error). (See AEI chart)

When you normalize for historical volatility (Z-Scores), the divergence vanishes

We"re miserable, and we know it. There is no "fake news" on the affordability crisis. I wrote on the topic of sentiment earlier this year in a piece called "Getting Sentimental" that identified it wasn"t traditional measures of economics that drove the collapse; it was trust.

I remain convinced that this is the real story " we no longer trust our leadership to work to make our lives better. (institutions)

So What DID Go Wrong?

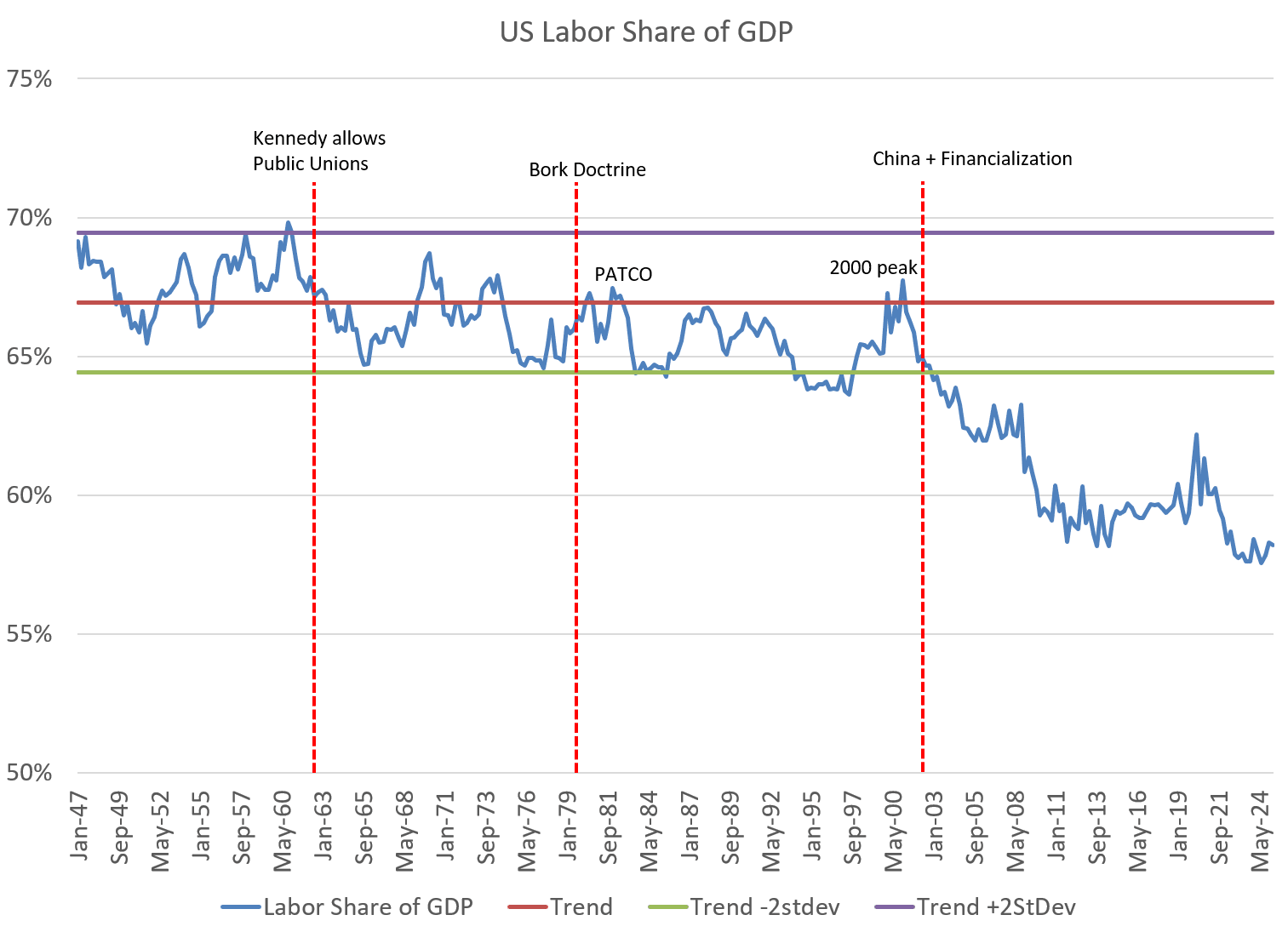

The single most important chart I can share is the following " the collapse in labor share of GDP.

You"ll obviously notice the three red lines. In my opinion, these are the structural changes that drove our "decline."

The first, Kennedy's Executive Order 10988, allowed the establishment of public labor unions. It was part of his deal with the AFL-CIO for support in the tight election of 1960

many states were beginning to make the transition. That wonderful NYC you"ve heard about from 1960-1990 [sarcasm] is largely a byproduct of this early move by Mayor Robert Wagner.

When Mayor Wagner granted bargaining rights to NYC public workers in 1958, he inadvertently ran an economic experiment: What happens when a monopoly provider of services (the City) negotiates with a monopoly provider of labor (the Union)?

-> erodes efficiency and raises costs without raising productivity.

In the private sector, efficiency is forced by the threat of competition and failure. In the public sector, that threat is theoretical"until it isn"t. The result was the 1975 fiscal crisis.

This leads us to our second red line " the Robert Bork Doctrine.

Before 1978, antitrust law focused on Market Structure

In his influential 1978 book The Antitrust Paradox, Robert Bork argued that this approach was actually anti-consumer

Competition" no longer meant a rivalry among many; it meant efficiency.

The Consequence: This effectively legalized corporate consolidation and consolidate they did:

some economists still defend the consumer-welfare standard, but virtually no one disputes that it reduced scrutiny of mergers and raised concentration across industries

as long as the company could promise lower prices at the checkout counter. And they kept that promise until the Covid-19 shutdown and subsequent demand surge gave them market power. (That's awfully recent for a symptom...)

corporations did not suddenly get greedy; they just found themselves in a position to exploit YOUR uncertainty. Should eggs be $3/dozen or $8/dozen? Hard to know when the price is changing daily. But you know who did know? Cal-Maine Foods

Here's an overview of how Cal-Maine Foods grew:

1. Founding and Early Growth (1969-1980s)

2. Strategic Acquisitions (1980s-1990s)

Acquisition Strategy: During the 1980s and 1990s, Cal-Maine pursued an aggressive acquisition strategy, purchasing numerous smaller egg producers across the U.S

3. Public Offering and National Expansion (1996-2000s)

...enabled the company to further its acquisition strategy and modernize its operations

National Presence: With the resources from the IPO, Cal-Maine expanded beyond the Southeast, becoming a national player in the egg industry

Adam Smith recognized that monopolies are the bane of competition " and the perfect tool to purchase politicians:

the next red line

the accelerators " the China Shock, when China was granted Most Favored Nation status, provided access to the WTO, and treated as an ally to America, and the financialization that became perverted by low interest rates.

Financialization

Government debt is a liquidity management exercise issued to "soak up" excess currency spent into the economy.

Who does finance themselves? Corporations and households. And there we find an explanation for credit crises " when nominal growth falls below corporate financing costs, corporates struggle to repay debt

In the 1980s and most of the 1990s, private equity was isolated to opportunities for restructuring where operating results would have to be improved to create "wealth." Since 2000, it has been a vehicle for levered financial speculation

this is not driven by low interest rates, per se, but rather by a combination of factors discussed above " consolidation, financial product dominance, and tax deductibility of interest. Low rates didn"t cause financialization, but they removed the final constraint on it. When leverage is cheap and tax-deductible, financial engineering reliably outperforms productive investment. Of course, low interest rates didn"t HURT the process" (ZIRP)

Astute readers will note that the current stresses in the credit markets are to be expected given slowing nominal growth. If a recession arrives, as it always does eventually, credit will be hit.

President Trump's solution? Cut interest rates. Mine? Accelerate REAL growth by addressing constraints.

The China Story

The story you THINK you know is that Chinese competition flooded the world with product; the real story is that Western capital flooded China and pulled off the greatest labor arbitrage

If you"re old enough to remember North Carolina's furniture industry collapse, you might note the resonance:

It happened so quickly. In just 10 years, between 1999 and 2009, North Carolina's furniture manufacturing industry lost more than half of its jobs. The chief culprit was increased competition from lower-cost furniture imported from Asia " mostly China.

One of the story's wrinkles is that the influx of Chinese imports had not been initiated by Chinese industrialists but rather by the North Carolina industry's own leaders, who had sought cost advantages that could put them ahead in what has historically been, and remains to this day, a highly competitive industry. " John Mullin

You want to know why you"re reading about China competition and tariffs now? It's no longer about jobs " it's about businesses that gave China the skills to compete under technology transfer and now can"t compete

President Bill Clinton famously argued that the deal was "a one-way street" in America's favor: "We import far more from China than we export to China. This agreement will open China's markets to us."

The primary selling point was that China represented the largest untapped market in human history. The narrative was that by lowering Chinese tariffs (which averaged 24% at the time compared to the U.S. 2%), American farmers, manufacturers, and service providers would gain unprecedented access to 1.2 billion new customers.

The good news is that we know the way to address this " tariff policy. This is also why a tariff realignment is uniquely viable today: globalization is unwinding, geopolitical blocs are forming, and capital mobility is no longer frictionless

many who benefit from this system don"t want to face the sacrifices that will be necessary. And they are happy to blame it on your unwillingness to accept higher prices. After reviewing the evidence, I believe this is false; Americans can accept hardship " they just need to understand why.

It's a repeating pattern: screw up the mortgage market and take the banks that sold undocumented mortgages into structured products? Bailout the banks and prop up home prices by lowering interest rates. Screw up in Covid? Stimulus to business that dwarfs stimulus to households. Screw up China? You know what's coming.

With the ascension of Xi in 2013, China surrendered any hope of becoming a free market economy. And one of the unfortunate facts you were not told by the "free marketeers" is that if Country A conducts free trade, while Country B suppresses the purchasing power (and freedoms) of their citizens to pervert comparative advantage, Country B will become the dominant producer. What did China buy? US treasuries " a good ole made in the USA product if there ever was one.

This leaves America to rebuild. And it can be done under two models " Americans as serfs, thankful for their lot in life, or Americans as free, told the truth and free to demand more of the rebuilding share. I know where my vote lies:

The Rule of 65 " my organizing principle

shifting taxes off workers and onto idle capital, forcing companies to invest through a 4-year capex shot clock, eliminating benefit cliffs, and restoring broad-based prosperity centered on the 65th percentile family

see stories that suggest tax policy doesn"t matter because US federal tax collections remain roughly the same percentage of GDP over time; this also has some truth to it:

But the simple reality is WHAT taxes are collected and who pays them has varied radically.

Who ACTUALLY pays taxes in the US? Well, you tell me:

So to summarize, the rich paid 39.2% of the 16.95% in 1955 and 31.8% of the 18.8% in 2025. As a percent of GDP, that's a decline from 6.64% to 5.98%.

You want to know why the elites decided to pick on my use of AI? Because they are scared. For decades they have flooded the news with stories of the unfair burdens of success on the rich. A general AI overview will answer the question accurately.

Just like with egg prices, confusion is their friend. Let's just be blatant about it and tell the truth: (see table)

They"re "right" " we don"t have a revenue problem" we have a SOURCE of revenue problem

And we also have a spending problem. We are spending money in the wrong places. High return? Spending on children. Low return? Lowering top tax rates isn"t a great idea, but even worse are government-directed expenditures (housing vouchers, SSI, Nutrition, Unemployment Insurance [Uber does it much better for now]). Adult health? Don"t get me started on hip replacements for 90-year-olds. (so he's a *conservative populist?)

My strong recommendation is to focus on expanding the earned income tax credit (EITC " a creation of Milton Friedman's that links work to expanded benefits lest anyone think I hate Uncle Milty) to give more CASH to households with young children while paying for it by uncapping FICA and lowering the FICA rate once the highest income earners are paying in.

Now for the proposal.

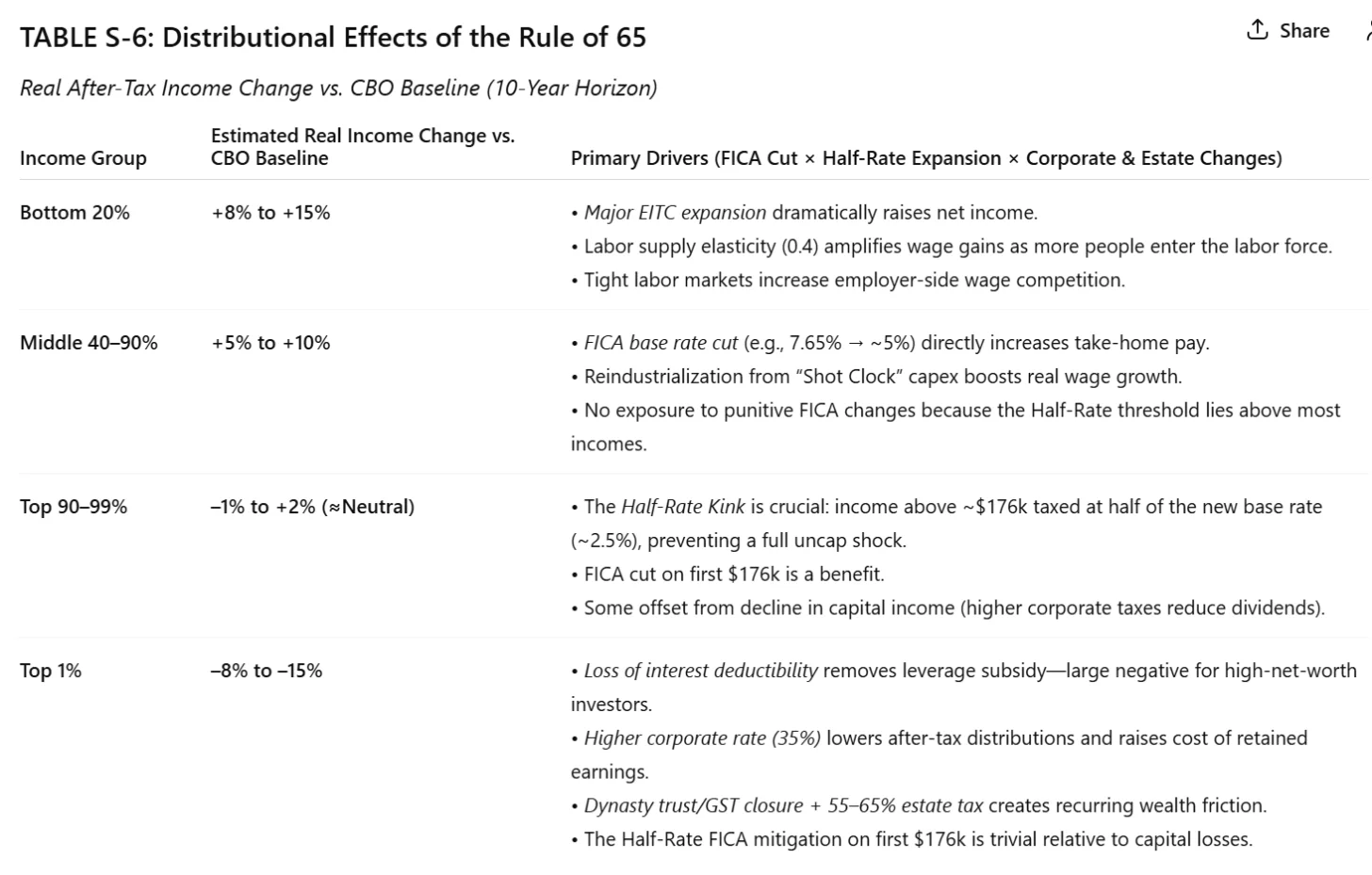

Readers, please copy and paste the below prompts into the LLM of your choice. I"ve tested it on ChatGPT, Gemini, and Grok. Be sure to query for areas of interest for YOU. As a general recommendation, request tables S-6, S-7, and S-8 from the LLM for a CBO-equivalent comparison. I would welcome comments evaluating your findings.

Here are my summary findings:

The "Rule of 65" Model Definition (v4.0) (see original)

Edited: | Tweet this! | Search Twitter for discussion

Made with flux.garden

Made with flux.garden